For many people, reducing or eliminating debt is an important part of improving their financial situation. If you have multiple revolving debt accounts, credit cards or lines of credit with variable interest rates, or loans at high interest rates, you may be able to pay off your debts sooner by combining all of the debts into one loan or credit card with a lower interest rate.

How do you decide what’s the best approach for your particular situation? We’ll break it down into 3 steps.

1. Examine your current payments:

For each loan, credit card, or line of credit you want to consider, gather the following information:

-

The total amount borrowed (the principle)

-

Interest rate

-

Term

For revolving debt like credit cards, the minimum payment each month usually includes 1–2% of the amount borrowed.

-

Minimum payment due each month

For revolving debt, be sure to note how much of your minimum payment each month goes toward the principle and how much goes toward interest. Most credit cards’ minimum payment is 1– 2% of the principle PLUS any accrued interest.

-

You might also want to calculate how much interest you will pay total over the length of the debt.

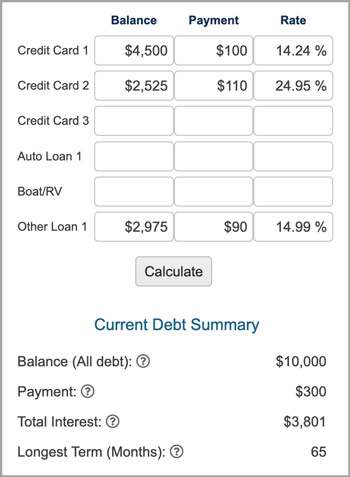

Calculate the total amount you pay now each month for all of these debts combined. Here's a sample of one person's debts:

2. Consider consolidation options:

At PSCCU, we have three primary options for helping members consolidate their debt: Personal Loans (Signature Loans), Home Equity Lines of Credit, and Credit Card Balance Transfers. You can take the debt information you gathered above and look at various consolidation scenarios using the Credit Calculators on our website or keep reading to see how each of these options play out for an imaginary member. Calculate the monthly payment, how long it will take you to pay off your debt, and the total amount of interest paid over the life of the loan. Hopefully, you will find an option with a lower monthly payment, shorter payment term, or both. Chose an option that suits your budget and helps you pay off that debt once and for all!

-

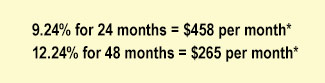

Signature Loan (Personal Loan): These loans enable you to pay back a set amount each month over a fixed term and with a fixed interest rate. That means your payment will be the same each month and cannot increase. Signature loans are available for up a 48-month term.

Using the example above of a person who owes $10,000, their monthly payments would look like this:

-

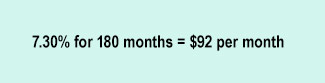

Home Equity Line of Credit (HELOC): If you own a home and owe less than it’s worth, you can leverage the difference (your equity) as collateral for a secured line of credit. Home Equity Lines of Credit are available for terms up to 15. A HELOC does have a variable interest rate so that rate may go up or down over time but since it’s secured by your home, the rate is typically lower than an unsecured loan or line of credit.

Using our example above of the person who owes $10,000, their monthly payments would look like this:

-

Credit Card Balance Transfer: While a loan with a low fixed rate (and no ability to take on additional debt) may be the preferred solution for some, a credit card balance transfer might make sense for others. PSCCU offers a Visa Platinum card with a fixed rate as low as 8.90%. Like with a HELOC, a credit card gives you some flexibility about how much you pay each month but, if your goal is to get out of debt, decide how much you are going to pay each month and stick to it!

Using our example above of the person who owes $10,000, a credit card balance transfer would look like this:

3. Beyond consolidation: Learning to live without debt

If you have been struggling to pay off revolving debt and are committed to moving beyond that phase of your life, once you consolidate your current debt into a single loan or payment plan, it’s key to not take on additional debt. You should consider closing your existing revolving debt accounts once the balance is transferred so that you don’t continue to take spend more than you can afford. In fact, you may find that your lender will make a consolidation loan to you only on the condition that you close the other accounts.